Dear readers,

Periodically, I receive messages from subscribers asking why I say only two U.S. airlines are pursuing a premium strategy. Surely, they allege, I must have a vendetta against American Airlines. Perhaps flight attendants failed to warm my mixed nuts the last time I flew in first class? Or maybe I’m tired of waiting for my interview with chief commercial officer Vasu Raja and I’ve decided to swipe at American’s onboard product every chance I get?

I can assure you: I don’t hate American Airlines, I’m fine with plane snacks of any temperature, and I look forward to talking with Raja whenever the time is right. I say it because it’s true — American is not pursuing the same premium strategy that Delta and United are, and if you still doubt me, well, read on.

On Monday, Raja spent his entire 30-minute spiel during American’s first investor day in seven years explaining exactly how American is conducting business differently than United or Delta.

As the other two engage in a premium arms race in large U.S. markets, American is focusing elsewhere, Raja said, deploying a good-enough product, plus what it views as an industry-leading loyalty program, as it tries to win travelers in smaller cities in Sunbelt states. I’m sure American’s new 787s — the ones with lots of business class suites — will be lovely, but Raja hardly touched on the airplane during his speech, because building a premium brand is not his focus. In fact, he bragged more about American’s enormous regional jet fleet than about premium products.

Many of you are skeptical about Raja’s approach. I am too. Though American focuses more on cost than its legacy network competitors (it has cut distribution expenses and laid off some contact center agents in recent months), American has roughly the same costs as its legacy network competitors, because labor and fuel are really expensive. And in recent history, United and Delta have sought to recoup those costs by persuading customers to pay more, through improving the onboard and airport product — not by bragging about how many one-stop markets they connect on regional jets from El Paso, as Raja did at investor day.

To his credit, Raja has had the same message for about five years, and he’s not wavering. You may think it’s the wrong plan — perhaps you’ll point to American’s margin gap to United and Delta as evidence — but at least we know Raja believes in it and can communicate it.

As he told analysts on Monday: “If we build a great network, if we reward customers for using it, if we do it reliably, and we deliver it efficiently, we grow value for our customers and for our investors alike.”

Let’s dig deeper about what that means.

For decades, United has had hubs in major Northern U.S. business cities, including San Francisco, Los Angeles, Chicago, Washington, D.C., and the Newark hub it inherited from Continental. Delta, which had been a predominately Southern airline, has built its Northern presence in the past couple of decades, wedging itself into strong competitive positions in New York, Boston, and Seattle. Delta still loves Atlanta, but president Glen Hauenstein also likes coastal markets for their juicy revenue and long-haul opportunities.

Raja says his competitors have it wrong, and he is all-in on the American South. On Monday he shared data that he argued proves his thesis. Between 2019 and 2022, he said, U.S. population in the Sunbelt rose 2.6 percent while it remained roughly flat in New York, Boston, Los Angeles, and in the San Francisco area. In addition, he said, Sunbelt states have higher economic growth rates compared to the nation’s average. “As the population is shifting, so too, the axis of economic growth is shifting,” he told investors. That helps American, he said, with its Sunbelt hubs in Texas, Arizona, Florida, and North Carolina.

But it’s not just the biggest markets in the Sunbelt. Raja likes smaller ones, too.

The largest 25 markets in the United States, including some in the Sunbelt, have plenty of air service. But Raja stressed that American’s Southern hubs allow it to access smaller markets that remain underserved, and that’s where the growth is. He told analysts that the smallest 200 U.S. cities that can support at least some air service, which “very often are the highest-growing cities in the U.S,” have significantly less capacity than before the pandemic. With fewer choices, these customers pay higher prices.

“Customers who are in those largest 25 cities tend to pay less than our system-average,” he said. “Those smallest cities pay materially more. … Demand is growing, and there’s an inadequate level of supply.”

Smaller market passengers will fly American, he said, because American will give them more options. “There is a large pool of high-growth, high-value customers whose air travel needs are simply not being met. That’s where American Airlines comes in.”

In the nation’s 200 smallest air markets, American captures a 163 percent yield premium over its system average, according to a slide. In the largest 25 markets, he said, its yield is about 98 percent of average.

If American were capturing 163 percent yield premium in one of its hubs — say, Phoenix, just as an example — that would be remarkable, because the operation there is so big. But therein lies the problem: many of these small markets American is prioritizing are closer to tiny than small.

“What we see today is that actually 60 percent of the airports in the United States have less than 500 passengers per day, each way, worth of demand,” Raja said. “For 60 percent of the airports in the United States, they couldn’t sustain multiple round-trip narrowbody service, per day.”

American earned $53 billion in total revenue last year, and while small markets may produce better unit revenue, we can reasonably assume from Raja’s comments that much of American’s revenue still comes from those so-so yields in big markets.

My good friend Brett Snyder of Cranky Flier looked at some of these markets in detail and called bullshit on Raja’s argument. Yes, Snyder wrote, some markets just outside of the top 100 have good demand, though he noted a lot of the more intriguing ones already are well-served, including by low-cost airlines. Beyond that, Snyder wrote, there’s probably some untapped potential, but not that much.

“To give you a sense, the largest of the ‘bottom 200’ markets is Tallahassee followed by South Bend and Charlottesville,” Snyder said. “Those are decent targets. But at the bottom end you have all those essential air service markets and other abandoned little markets that simply are not ever going to be viable. The idea that there are 200 markets with endless opportunity for American at the bottom end is silly and overstates the actual opportunity… mid-size cities.”

Good presentations have concrete examples, often using cherry-picked data that fits the thesis. Raja found his in El Paso, where American flies 14 peak-day departures to hubs at Dallas/Fort Worth, Los Angeles, Phoenix, and Chicago. Raja claims this schedule is twice as large as United’s, and seven times as large as Delta’s, though Snyder points out the competition uses larger (and lower unit cost) airplanes with more seats.

There’s also considerable competition with Southwest, though Raja said the better comparison is United and Delta, because, like American, both claim to connect cities like El Paso to the world. And compared to them, Raja said, American’s schedule breadth creates more connections.

“What American Airlines uniquely does is we’re able to get customers from El Paso to Louisiana; and El Paso to Montgomery, Alabama; El Paso to Mexico City; and El Paso to Madrid, Spain,” he said. “If you are a high-growth customer in El Paso, you will tend to prefer American Airlines” over a ULCC or another network carrier.

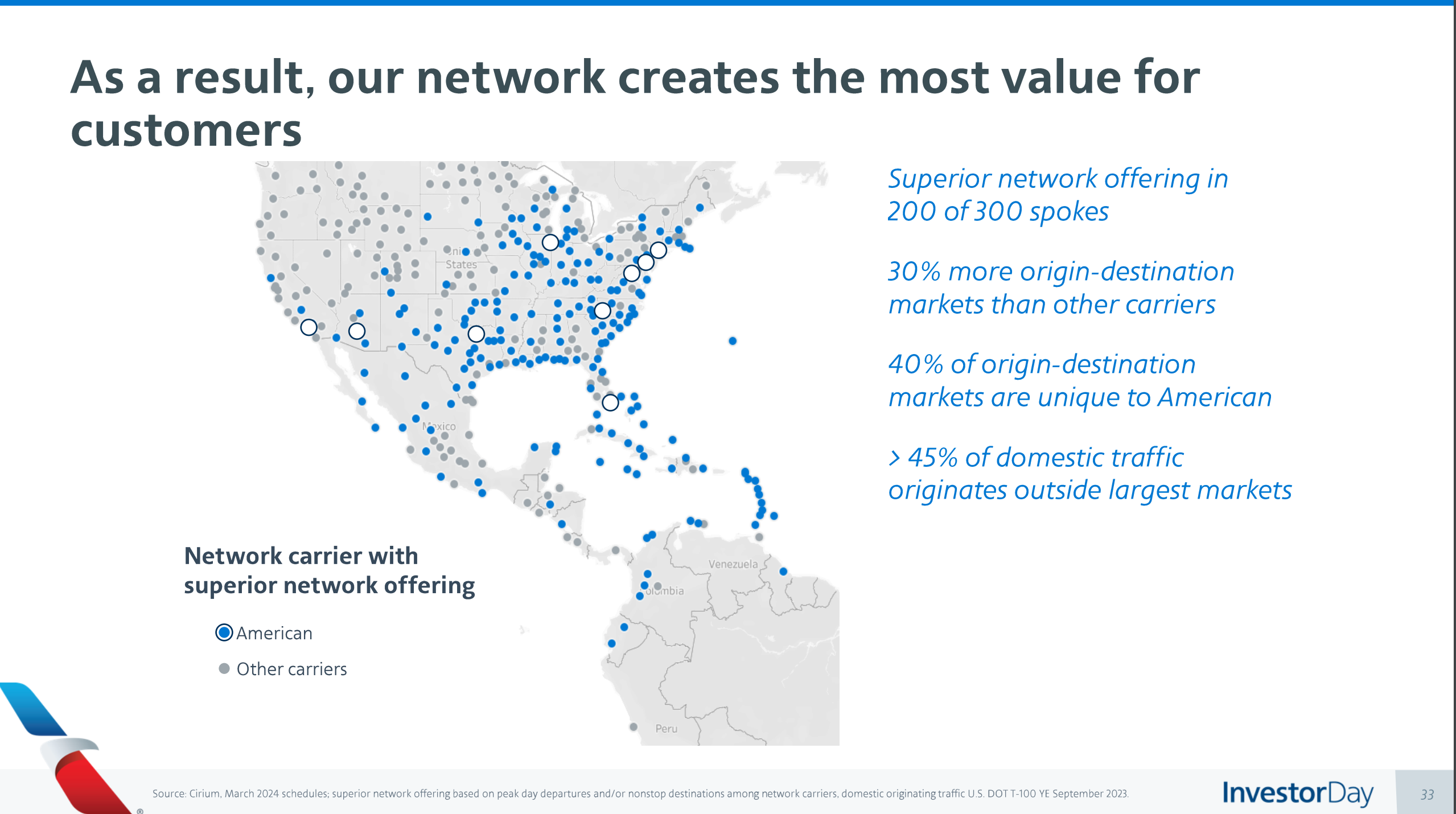

Raja said he has found many more markets where American has a network advantage and can create more connections than Delta or United. Of 300 key markets in the Americas with air service, American claims it has a network advantage in 200. As recently as 10 years ago, American had a network advantage in only half of these 300 markets, Raja said.

It does, and as you know, these airplanes typically are expensive to operate. The Embraer 175 has better unit costs than most regional jets, but the airplanes are still costly on a per-seat basis, which is why United and Delta up-gauge where possible. But Raja argues that the industry has overcorrected, and that the 556 regional jets in American’s fleet at the end of 2023 — 210 of which were E175s — give him a competitive advantage.

“It is a very compelling and competitive product,” Raja said on Monday. “Importantly, it’s also a very efficient one. When our 75-seaters compete against one of our competitors’ 175-seat narrowbody jets, we are competing with the 60 percent trip cost advantage to what they have. Also, we have 50 percent more regional jets than what our next largest competitor has.”

It does, but perhaps not as many as in the past.

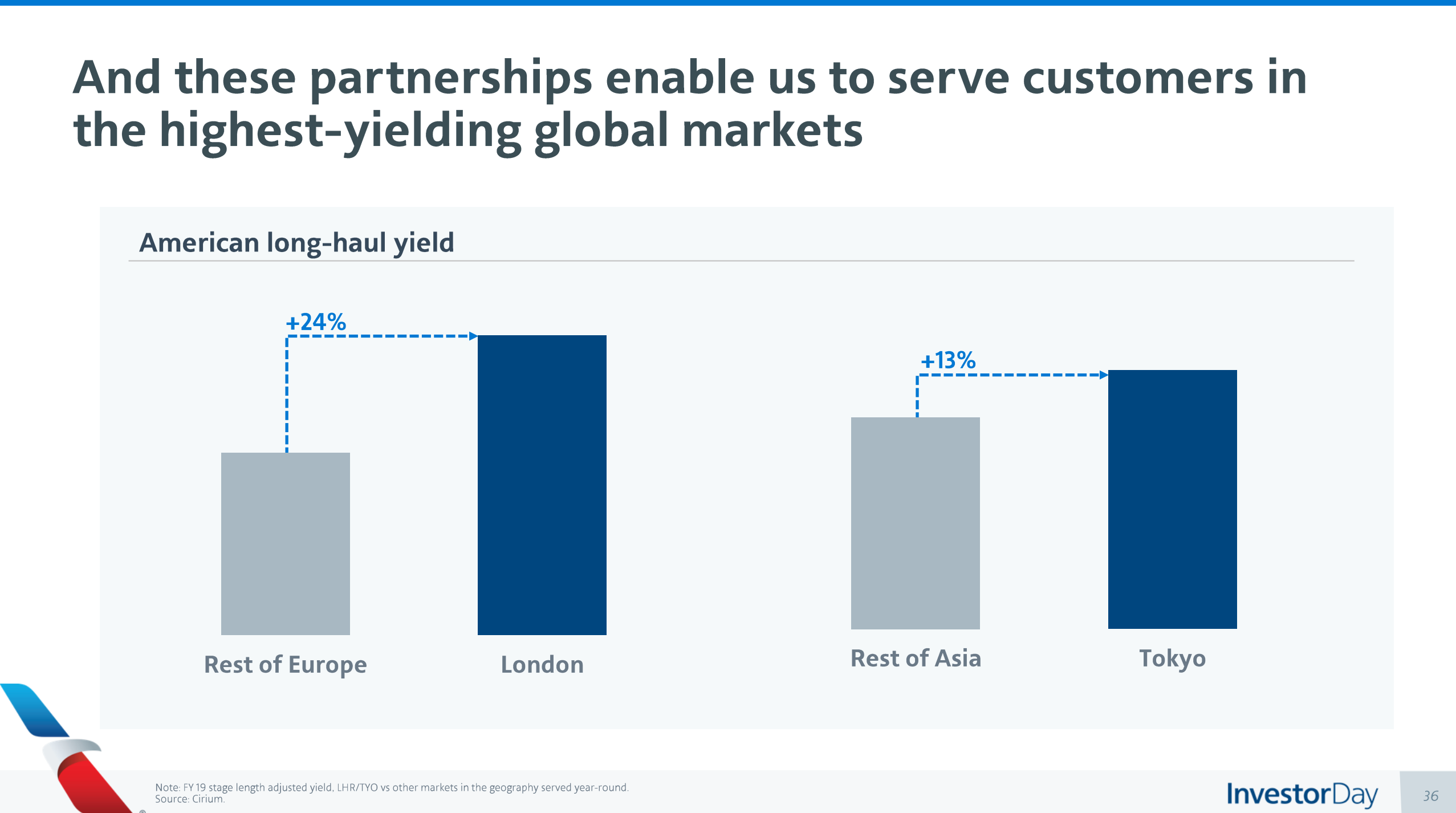

Raja makes no secret of American’s long-haul plan: Outside of its summertime Europe network and its Latin America franchise, it likes to fly to partner hubs, because building a new route is hard and flying to London and Tokyo is low-risk.

“When we’re talking about growing to India, we’re talking about deploying $200 million of flight assets to go into a market,” he said. “Through our partnerships, we get to see customer demand and we get to actually sell that demand before we enter it, greatly de-risking market entry.”

Raja noted that neither London nor Tokyo has anywhere near the level of connectivity as other hubs in their regions, because they’re such robust O&D cities. But he said both markets drive a yield premium for American nonetheless, because “we’ve constructed these partnerships to be durable.”

Raja teased some European point-to-point growth once American’s Airbus A321XLRs arrive in the next couple of years, saying that it’ll be an excellent airplane to fly from the East Coast to Europe. He said he likes it because it solves a problem that long has vexed American — what to do with a Philadelphia-based long-haul airplane in the winter.

“When demand starts to wane in the North Atlantic, we can take the exact same airplane and fly it in the U.S. transcon [market], where it has a 15 percent revenue premium to a typical domestic-configured 321 airplane,” Raja said.

American may have a network edge in some places, but it still competes with Delta and United in many markets. So if not on product, how will Raja ensure that customers opt for American?

He’s betting American’s loyalty program can shift share, and he’s promising to make it more rewarding for customers. Yes, whenever we hear of a U.S. airline promising to “enhance” its award travel program, we typically expect a major devaluation. Delta has been doing this for awhile, making its award currency less valuable, and United has been following, though not as drastically. There are several reasons why both airlines have felt confident in raising award prices, but a big one is this: When an airline offers a premium experience, people will pay for it even if they won’t earn a free business class ticket after four or five paid flights.

American is a bit of a throwback with its philosophy. It isn’t going to compete on product, but in Raja’s words, “we are very much focused on building the world’s best travel rewards program.” And yes, I believe him, because an airline can’t rely on a captive audience for all of its revenue.

“We’ll create more opportunities for customers to go and redeem miles at very high value per mile,” he said. “Our true north … is that life is better as an AAdvantage customer. It is our only commercial focus, and it as turned into three very core principles that we hold dear — it should be easy to earn miles and be our customer; we should offer the highest value per mile of any rewards program there is; and our status benefits should be unique and unmatched.”

Of course it is. With a more valuable program, Raja is betting more people will want to earn the currency, and one of the best ways to do that is by spending on credit cards.

Today, roughly 6 percent of U.S. air travel customers have an American co-brand credit card, while 23 percent of U.S. air travelers have an AAdvantage account.

“We have significantly more opportunity to just acquire people who look like the ones that we have, and do better with the customers that we already have,” Raja said.

American is renegotiating a credit card deal for the first time in a decade, Raja said, and the airline is salivating at the revenue prospects. The airline is talking to banks, including existing partners at Citi and Barclays, about the economics, Raja said. In recent years, American has been growing revenue from bank deals by about 7 percent annually, but in the future, American is targeting 10 percent.

“We have a network which uniquely addresses customers in a very high-growth, high-value segment,” Raja said. “We have AAdvantage, which makes their lives better and rewards them for buying higher value products and services. And we have a very bold vision for what our card can be. We envision a partnership with a bank that can create the largest branded credit card in circulation.”

That’s all for today. Thank you for reading. And since this post is free, I expect more people will find. it. Have questions about The Airline Observer? Want information about a discounted group subscription? Send me an email.