Weekly highlights

- Asia-US West Coast prices (FBX01 Weekly) fell 4% to $4,244/FEU.

- Asia-US East Coast prices (FBX03 Weekly) fell 4% to $5,875/FEU.

- Asia-N. Europe prices (FBX11 Weekly) fell 10% to $3,871/FEU.

- Asia-Mediterranean prices (FBX13 Weekly) fell 7% to $4,155/FEU.

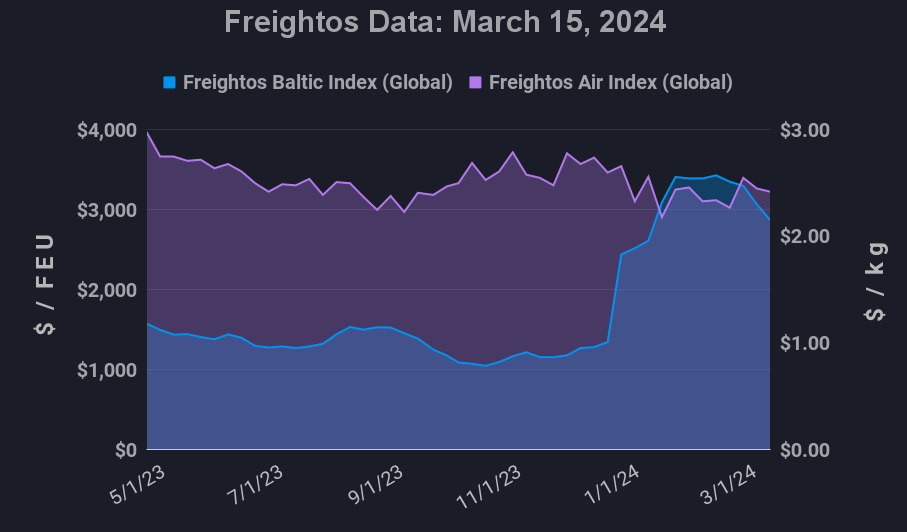

- China – N. America weekly prices increased 50% to $5.94/kg.

- China – N. Europe weekly prices increased 32% to $3.93/kg.

- N. Europe – N. America weekly prices increased 3% to $2.15/kg.

Dive deeper into freight data that matters

Stay in the know in the now with instant freight data reporting

Analysis

In the latest development in the Red Sea crisis, Houthis recently announced threats to expand their attacks to Indian Ocean traffic, aimed at disrupting vessel flows already diverting away from the Red Sea toward the Cape of Good Hope.

In the meantime, with most container traffic already avoiding the Suez Canal, demand easing, and operations stabilizing, ocean rates continued to decrease across the major tradelanes.

Weekly rate averages out of Asia last week fell another 7% to N. America and 7-10% to N. Europe and the Mediterranean. Prices have continued to drop so far this week with rates to N. America West Coast now 24% lower than its February peak, and prices to N. Europe and the Mediterranean 30% lower than their respective peaks in late January.

Most observers expect rates to remain well above normal levels while diversions continue, as carriers are facing higher costs and the longer routes soak up capacity. Still, current rates are around 2.5X their levels in 2019, suggesting there may be further to fall before prices settle at a new, elevated floor.

Optimistic N. American demand projections could also help keep N. America rates above normal, with carriers reportedly adding capacity for the coming month in anticipation of improving volumes. Easing Panama Canal restrictions announced last week – which will increase daily transits to 27 – are also a good sign for transpacific shippers to the East Coast. However, concerns over the looming October deadline for the East Coast and Gulf port worker union and port operators to reach an agreement may pull some demand to the earlier months of peak season this year or shift some volumes to the West Coast, though many are hopeful that labor disruptions can be avoided.

Though ocean flows out of India are improving, there is still additional pressure on air cargo in the region which started in late January due in large part to Red Sea-driven disruptions, with demand for sea-air out of Dubai also still elevated. Freightos Air Index rates out of S. Asia reached $4.60/kg to N. America last week, 55% higher than in December, with prices to Europe nearly double their end of year level at $3.55/kg.

Demand out of China has also climbed in the last couple weeks, with growing e-commerce volumes one factor. Rates reached $5.94/kg to N. America and $3.93/kg to N. Europe last week. American passenger carriers opting to still not fully restore weekly schedules to China due to lagging tourism demand may also represent some capacity restraint for this lane.

Freight news travels faster than cargo

Get industry-leading insights in your inbox.