Last time, we discussed accounting for blockchain staking income from the perspective of blockchain network validators. Today, we will talk about accounting for delegators.

Delegators are holders of digital assets who assign their tokens as a stake to a validator. See details in my previous post:

It’s crucial to stay informed about accounting requirement changes. Different jurisdictions may have unique requirements for reporting staking income, and staying compliant ensures your practices remain up to date. Our discussion here is limited to US GAAP. Now let’s dive in.

Accrued Staking Rewards

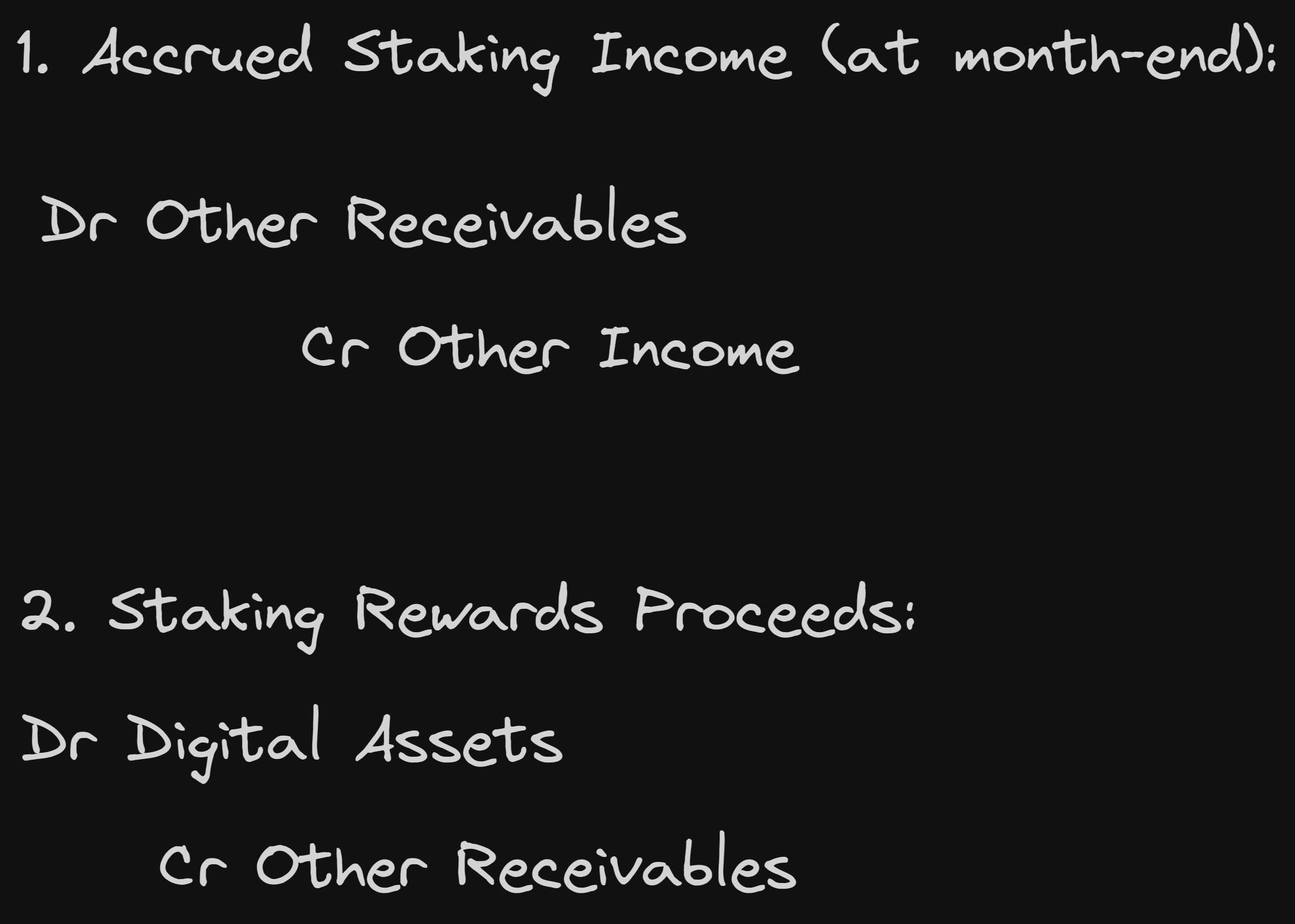

Sometimes, staking rewards are directly observable on the blockchain as receipt transactions. However, not always. Some staking rewards are not recorded on chain until the time when the rewards are paid out. Such rewards are calculated within the smart contract based on the input parameters defined in the staking smart contract code. The balance of rewards in a smart contract can be queried at any time, but in 99.9% the historical balance as of specific date cannot be queried. Similarly, some blockchain explorers do not reflect recurring validator rewards traced alongside other transactional activities on the account. This means that sometimes, the only way to learn your balance of unclaimed rewards is to make a contract call to read your balance precisely at the end of the period. As a result, to track and prove the existence of the balance, accountants need to capture screenshot data exactly at the end of accounting period and calculate the accrued income (in tokens) for the period by balancing the beginning and ending balance with receipts during the period:

By analogizing the accounting requirements with ASC 606, we can use the price at the staking contract inception date as the basis for calculating the dollar amount of staking income. Because duration of staking contract is highly dependent on specific terms and arrangements, the frequency of price updates may vary significantly.

Some blockchain protocols reduce the rewards delegators receive by imposing so-called community “taxes”. However, assuming the delegator account for staking income on a net basis (based on the reasons explained in the next section), no adjustments needed to separately account for these deductions on a gross basis.

Staking Income Presentation

From the perspective of delegators, the DeFi or blockchain protocol is not (usually) a customer. This means delegator rewards should be included in other income rather than revenue. There are a few exceptions:

-

When the company acts as both delegator and validator on a network and delegates owned/leased/borrowed tokens to self-stake on its validator node,

-

When the protocol is, in fact, treated as a customer of the company.

I also note that as delegators do not control the service provided, they always present income on a net basis. However, since we present the staking income in the “Other income (expenses), net” line item that is always presented on a net basis, this is not relevant to us due to the tradition to always present “Other income (expenses)” on a net aggregated basis.

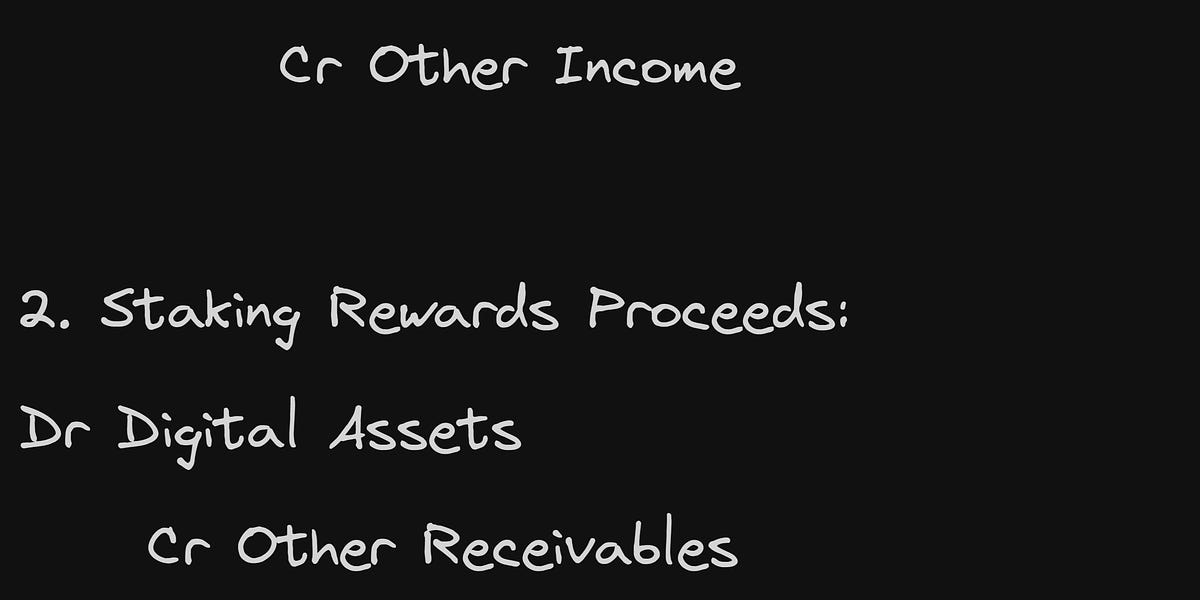

Accrued (Unclaimed) Rewards

On the corresponding debit side of this entry, we will account for accrued rewards as other receivables, unless the staking rewards is from the arrangement with a customer.

In arrangements with customers, the accounting will depend on whether these rewards are forfeitable or not as follows:

-

Forfeitable unclaimed rewards should be debited as contract assets because the time passage is not the only condition necessary to have an enforceable right on accrued rewards (because the delegator’s right on unclaimed rewards is also dependent on whether these rewards were claimed or not).

-

Non-forfeitable unclaimed rewards may be viewed as either account receivable because although the claim is required to receive rewards, this requirement is not substantive and late claim does not remove the delegator’s eligibility to receive rewards.

Accounting for blockchain staking income for delegators involves understanding the nuances of accrued staking rewards, proper income presentation, and accurately recording transactions. By following the outlined practices, including the correct treatment of unclaimed rewards and adhering to evolving regulatory standards, delegators can ensure their accounting practices are both accurate and compliant.

I hope this guide clarifies the process of accounting for staking income for delegators. Have you encountered challenges or have additional insights on this topic? Share your experiences and questions in the comments below. Your input can help our common understanding of accounting practices.