In this post, I will use the term “Environmental Credit Assets” (ECA) to encompass both carbon credit offsets and renewable energy credits. However, I do want to emphasize that these are two different things. You can find each definition below:

Carbon Credit Offsets are certificates that show a reduction in greenhouse gases equivalent to one ton of carbon dioxide, used to balance out emissions made elsewhere.

Renewable Energy Credits (RECs) are certificates showing that one megawatt-hour of electricity was generated from a renewable source, like wind or solar, helping to reduce reliance on fossil fuels.

I also want to ask you to take a look at this MorningStar publication [4], which talks about the difference between the two terms. Now, with this taken care of, let’s turn to the actual topic of this post. My goal today is to highlight a contradiction in existing accounting rules related to the US GAAP accounting for environmental credit assets vs. digital assets.

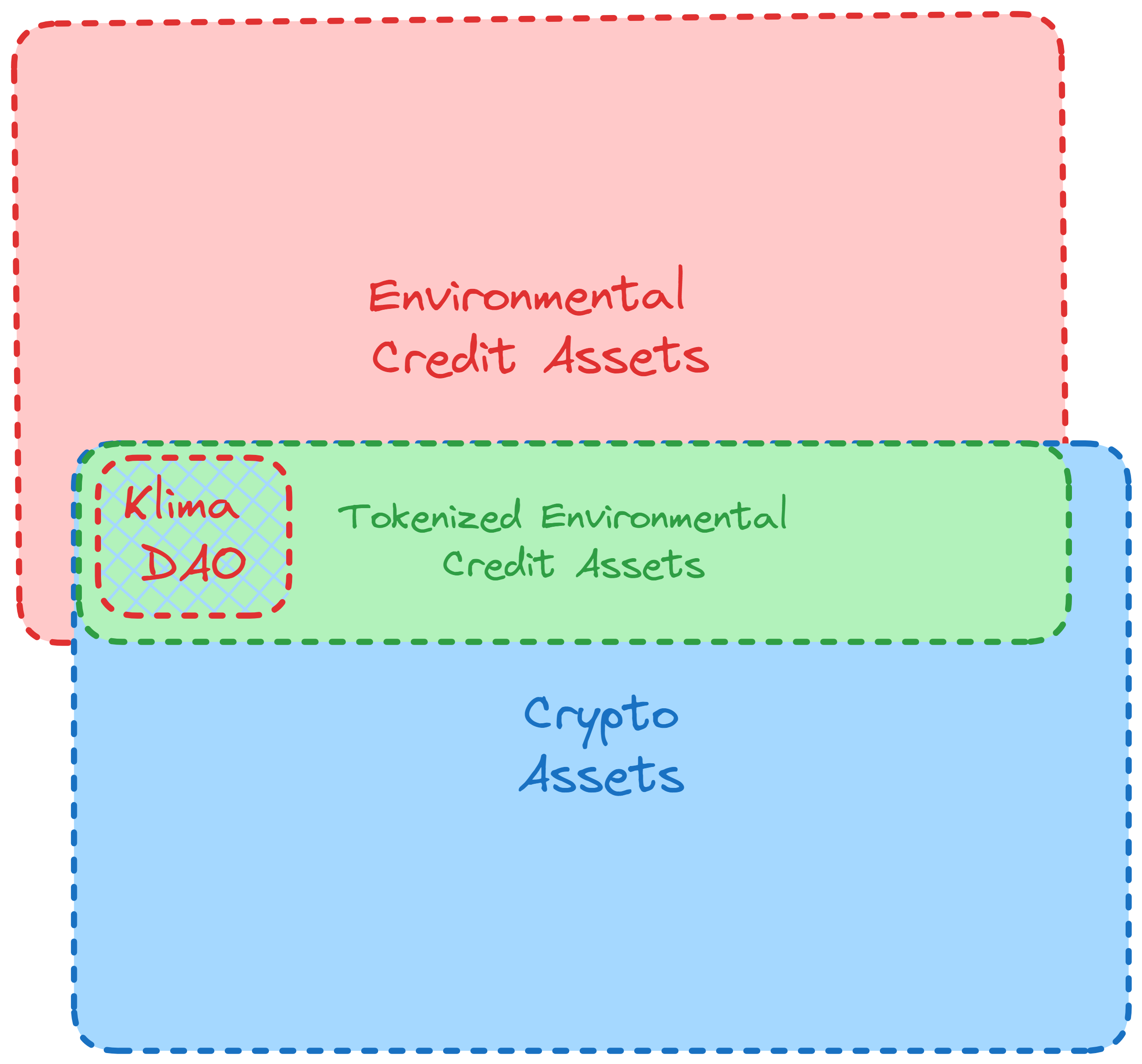

Neither digital assets nor environmental credit assets have a physical form. From this perspective, both types of assets are intangible. Furthermore, some environmental credit assets are being issued as blockchain tokens (e.g., the KlimaDAO token).

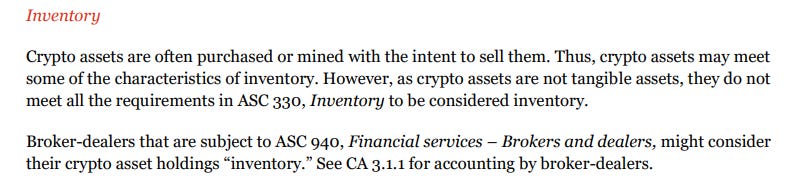

There are two approaches to accounting for environmental credit assets described by Deloitte and FEI:

“In informal and industry-related discussions, the FASB and SEC have indicated that two methods of accounting for emission allowances are acceptable:

(1) an inventory model and

(2) an intangible asset model.

In practice, entities generally select an accounting model based on the intended use for the environmental credits. For instance, when an entity plans to actively trade its environmental credits, it often accounts for them under an inventory model.” [6], [7]

In the Power & Utilities guide by PwC [5], we can further find a list of three scenarios where the inventory classification may be appropriate based on the intended use:

-

Entities engaged in generating and selling ECAs;

-

Entities engaged in buying and selling ECAs in the normal course of business;

-

Entities that purchase ECAs to comply with regulatory requirements.

In practice, these three scenarios encompass any entity that produces, purchases, sells, or retires ECAs regularly as part of their business.

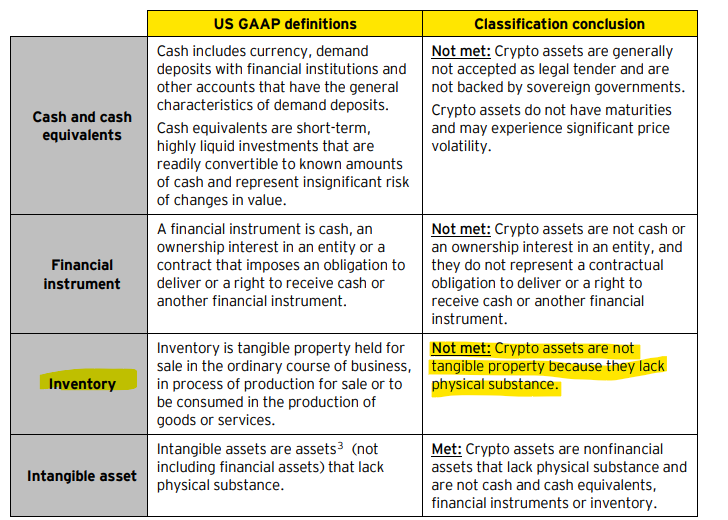

Generally, crypto assets accounting is guided by FASB ASC 350-60. However, the scope of this guidance excludes any blockchain tokens that provide the asset holder with enforceable rights to or claims on underlying goods, services, or other assets. Based on the website of KlimaDAO, we can find that environmental credit assets back the $KLIMA token, and each $KLIMA token can be used to retire the underlying environmental credit assets via the KlimaDAO retirement aggregator. Therefore, $KLIMA is out of the scope of ASC 350-60.

If the guidance for crypto assets does not apply to a token, we are basically being thrown back to the time when there was no guidance on accounting for crypto assets. However, when a digital asset merely represents another underlying asset, the accounting is based on requirements that apply to the underlying asset. In the case of KlimaDAO, each $KLIMA represents environmental credit assets that may be accounted for as inventory (as discussed above) if the company regularly produces, purchases, sells, or retires ECAs as part of its operations.

Now, this conclusion is particularly interesting to me. Because it contradicts these big-4 guides on accounting for crypto assets:

Thank you for reading this blog post. Stay tuned for the upcoming materials.

[1] ISDA. (2023). “Accounting for Carbon Credits”

[2] PwC. (2021). “Accounting for your company’s zero-carbon future”

[4] MorningStar (2023). “Carbon Offsets vs. Carbon Credits: What’s the Difference?”

[5] PwC. (2016). “Utilities & Power Guide”.

[6] FEI. (2022). “What to Know About Accounting For Environmental Credits”

[7] Deloitte. (2022). “Accounting for renewable energy environmental credits”