Banks of all sizes should be familiar with the evaluation standards under the Retail Lending Test, which will account for 40% or more of a bank’s overall performance rating. The test is mandatory for large and intermediate banks, but optional for small banks. The CRA modernization rule includes some familiar concepts, such as comparing the bank’s performance to demographic and market data. It also introduces many new concepts such as a retail lending volume screen, weighted factors and specific thresholds based on demographic and market data to obtain a given rating.

KEY TAKEAWAYS

- What impact the Retail Lending Test has on banks of all sizes

- How the Retail Lending Test impacts evaluation in facility-based assessment areas, retail lending assessment areas and other retail lending areas (ORLA)

- What role the retail lending volume screen plays in determining a bank’s overall performance rating

- Distribution analyses for LMI census tracts and LMI borrowers

- Distribution analyses for businesses and farms with gross annual revenues of $1 million or less

WHAT IMPACT DOES THE RETAIL LENDING TEST HAVE ON THE BANK’S OVERALL CRA RATING?

Please note that small banks are institutions with total assets of less than $600 million. Banks that have total assets of at least $600 million but less than $2 billion are considered intermediate. Large banks are those with total assets of $2 billion or more.

Small Banks will be evaluated under the current or “legacy” criteria unless they opt-in to the Retail Lending Test. For those that do opt-in, the Retail Lending Test will consist of the entirety of their rating.

Intermediate Banks will be evaluated under the Retail Lending Test and either the legacy community development test or the new Community Development Financing Test if they opt-in to the new test. Regardless, the Retail Lending Test will account for 50% of the overall rating with a minimum rating of Low Satisfactory required to obtain an overall Satisfactory or Outstanding rating.

Large Banks will be evaluated under the Retail Lending Test, which will account for 40% of the overall rating, with a minimum rating of Low Satisfactory required to obtain an overall Satisfactory or Outstanding rating.

WHICH GEOGRAPHIC AREAS WILL BE EVALUATED UNDER THE RETAIL LENDING TEST?

Facility-Based Assessment Areas (FBAA) are similar to legacy assessment areas and include the bank’s physical locations and deposit-taking remote service facilities. One change from the legacy assessment areas is that for large banks, FBAAs must consist of entire counties. Intermediate and small banks may still delineate partial counties as appropriate.

Retail Lending Assessment Areas (RLAA) are only required for large banks when less than 80% of retail lending occurs outside of their FBAAs. RLAAs consist of those metropolitan statistical areas or non-metropolitan areas of a state outside of a bank’s FBAAs that include at least 150 closed-end home mortgage loan originations or 400 small business loan originations in each of the two previous calendar years. Intermediate and small banks are not required to delineate RLAAs.

Outside Retail Lending Areas (ORLA) are those areas nationwide where lending occurs outside of an FBAA or RLAA. ORLAs are evaluated for large banks. For small banks that opt-in to the Retail Lending Test and for intermediate banks, ORLAs will be evaluated at the bank’s option or if more than 50% of retail loans were originated or purchased outside of the Bank’s FBAAs in each of the prior two calendar years. ORLAs will factor into the rating at the institutional level by component areas consisting of an MSA or nonmetropolitan area of a state.

WHAT IS THE RETAIL LENDING VOLUME SCREEN?

The Retail Lending Volume Screen measures the volume of a bank’s retail lending relative to its deposit base in FBAAs and in comparison to other banks with a physical presence within the FBAA. The Retail Lending Volume Screen does not apply to RLAAs or ORLAs.

The Bank Volume Metric is calculated by adding the bank’s originations of both closed- and open-end home mortgage loans, multifamily loans, small business loans, small farm loans and automobile loans, if applicable, for each year of the evaluation period. Then you divide that total by the sum of the deposits attributed to the FBAA for each year of the evaluation period.

The Market Volume Benchmark is a similar aggregate ratio for all benchmark depository institutions with a facility located in the bank’s FBAA. The Retail Lending Volume Threshold is equal to 30% of the Market Volume Benchmark. For example, if the Market Volume Benchmark is 40%, then the Retail Lending Volume Threshold is 12%. A Bank Volume Metric that doesn’t meet or surpass the Retail Lending Volume Threshold could prevent a Satisfactory rating in an FBAA unless factors such as the bank’s business strategy, safety and soundness limitations, etc. sufficiently mitigate this initial concern.

WHAT TYPES OF DISTRIBUTION ANALYSES WILL BE PERFORMED?

The four potential Major Product Lines that will be evaluated for FBAAs and ORLAs are closed-end home mortgage loans, small business loans, small farm loans and automobile loans, if applicable. Any of these product lines that constitute 15% or more, based on an average number of loans and dollar volume, of loans across all product lines in the FBAA or ORLA during the evaluation period will be evaluated.

RLAAs will only be evaluated on closed-end home mortgage loans if reported originations numbered at least 150 in each of the two previous calendar years. Small business loans will be evaluated if reported originations numbered at least 400 in each of the two previous calendar years.

For each product line, the Geographic Distribution Analysis will separately compare the bank’s level of lending in low-income census tracts (CT) and moderate-income CTs to Market and Community Benchmarks. Market Benchmarks are the level of all reporting lender’s originations in the FBAA, RLAA, or ORLA that were made in CTs of similar income level. Community Benchmarks are demographic data, such as the number of owner-occupied housing units, small businesses or small farms within CTs of similar income levels within the FBAA, RLAA or ORLA.

Similarly, the Borrower Distribution Analysis will separately compare the bank’s level of lending to low-income and moderate-income borrowers, to businesses or farms with gross annual revenues of $250,000 or less and to businesses or farms with gross annual revenues from $250,001 to $1 million to corresponding Market and Community Benchmarks.

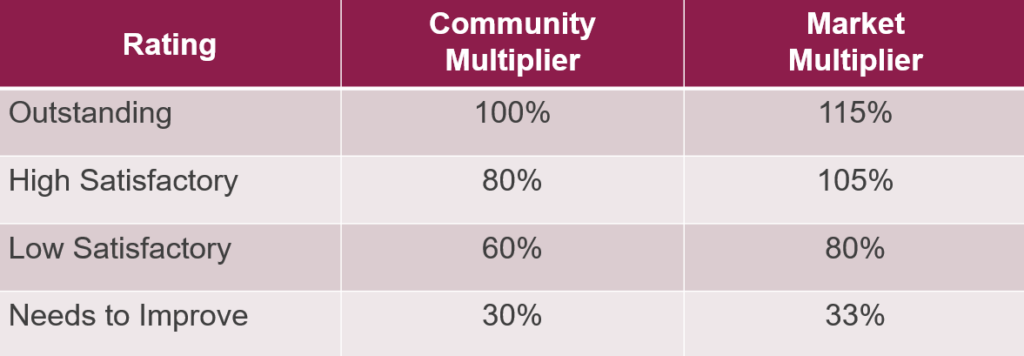

Thresholds for obtaining a given rating are then calculated by multiplying the benchmark by a multiplier, as demonstrated in the following table.

For example, if 12% of benchmark home loans originated in low-income CTs, then the calibrated Market Benchmark to obtain an Outstanding rating for that analysis would be 13.8% (12% x 115%).

Similarly, if 16% of owner-occupied housing units were in low-income CTs, then the calibrated Community Benchmark to obtain an Outstanding rating for that analysis would be 16% (16% x 100%).

The lower of these two calibrated benchmarks, 13.8% in this example, then serves as the threshold to obtain an Outstanding rating for that analysis.

This process is then repeated for each of the four distribution analyses for each Major Product Line in each FBAA, RLAA and ORLA.

HOW ARE VARIOUS ASPECTS OF THE EVALUATION WEIGHTED?

Each aspect of the analysis is then weighted. For example, if there are 60 owner-occupied housing units in moderate-income CTs and 40 in low-income CTs, then home lending in moderate-income CTs would receive a 60% weighting factor and home lending in low-income CTs would receive a 40% weighting factor for that FBAA, RLAA or ORLA. Similar weighting factors would be assigned to each aspect of the Distribution Analysis based on appropriate Community data. Each product line in the FBAA, RLAA or ORLA is then assigned a Product Line Score that is the average of the weighted performance score for the geographic and borrower distribution analyses.

The Product Line Scores are then weighted based on an average percent of that product line within the FBAA, RLAA or ORLA based on the number and dollar volume of loans. For example, if small business loans represented 60% of loans by number and 40% by dollar volume, the weighting factor would be 50% ((60+40)/2).

Once a rating has been determined for each FBAA, RLAA and ORLA, then the ratings for each of these areas are weighted based on an average of the percent of deposits and loans during the evaluation period that are assigned to the area. For example, if an RLAA accounted for 8% of deposits and 68% of loans, then its weighting factor would be 38% ((8+68)/2).

Similar concepts would be followed when determining ratings at the MSA, state and institutional levels. At various stages throughout the process, the recommended rating determined through these numeric processes can be adjusted based on additional factors and performance context. For example, the purchase of loans for the primary purpose of enhancing a bank’s CRA performance could result in those loans not being considered in the evaluation. Or lending in underserved or distressed nonmetropolitan CTs could be considered an FBAA, RLAA or ORLA with few or no LMI CTs.

Anders Banking and Financial Institutions advisors work closely with the lending industry to maintain compliance with federal regulations. Our advisors monitor evolving regulations and legislation to ensure your institution is properly prepared for the changes ahead. To learn more about our services, and the associated costs, request a meeting with an Anders advisor below.

Discover more from reviewer4you.com

Subscribe to get the latest posts to your email.