Powell makes it clear: No rate cuts anytime soon

Powell: “Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work and let the data and evolving outlook guide us.”

The Fed believes the labor market has been too firm, and wages have been growing too fast. By attaching the labor supply, the Fed believes Americans will make less money, forcing them to spend less. However, they’ve always wanted the labor market to break, meaning jobless claims rising, before they can give the A-OK to pivot. I brought this up last year in a CNBC interview. However, with the recent inflation data that has come into play, the Fed believes it’s too much of a risk to cut rates now while the labor market is intact.

Powell: “The performance of the U.S. economy over the past year has really been quite strong. We had growth of more than 3% last year as rebounding supply supported both robust growth in spending and also employment alongside a considerable decline in inflation. More recent data shows solid growth and continued strength in the labor market but also a lack of further progress so far this year in returning to our 2% inflation goal.”

Regarding this statement, the labor market has gotten softer based on their models, but it hasn’t broken yet. There is a difference between getting softer versus breaking. In this article I show a lot of charts and explain why they could land the plane if they wanted to do so. As this comment shows, the goal is for the labor market to break; it hasn’t yet.

Powell: “The labor market remains very strong…the unemployment rates has been below 4% for 26 consecutive months which hasn’t happened in more than half a century, the longest streak of its kind.”

Regarding the labor market, we want to keep this simple as we have talked about it since 2022. The labor market breaking means jobless claims rising. When jobless claims rise, the Fed will take notice, as they said in the recent Fed press meeting. However, they see the low jobless claims as a reason for them to still be restrictive.

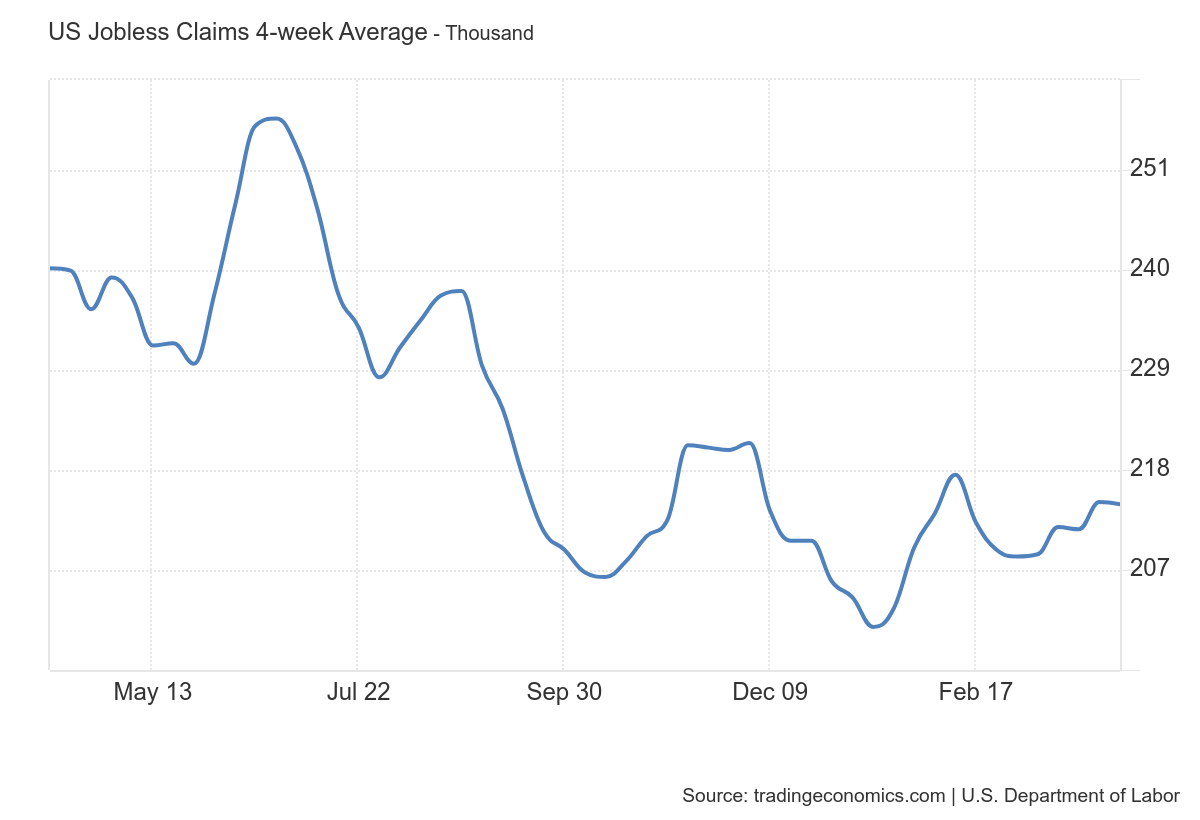

Currently, jobless claims on the four-week moving average are at 214,000. I believe jobless claims would need to rise to 323000 on a four-week moving average for the Fed to pivot.

Powell: “We’ve said at the FOMC that we will need greater confidence that inflation is moving sustainably toward 2% before it would be appropriate to ease policy… The recent data have clearly not given us greater confidence and instead indicate that its likely to take longer than expected to achieve that confidence.”

This just proves to me that the timeline for rate cuts will change not based on inflation but by the labor data getting weaker. If the labor market breaks, the Federal Reserve won’t need time to think about it — they just need to see enough people losing their jobs.

The main point of today’s remarks is that the recent economic data is too strong for the Fed to make rate cuts. The economy is growing above trend, retail sales just came in as a big beat, and jobless claims are too low. For those reasons — and the fact that recent inflation data is sticky — the Fed will hold off on any rate cuts until they see more weakness in the economic data or the labor market. I believe that if the labor market was breaking today, they wouldn’t care so much about the recent inflation, but jobless claims are simply too low.

Discover more from reviewer4you.com

Subscribe to get the latest posts to your email.