Under ASC 606 we apply the 5-step revenue recognition model:

Steps 1-3. Identify:

• the contract with a customer

• performance obligations (promises given to the customer),

• the total transaction price,

Step 4. Allocate:

the transaction price among performance obligations,

Step 5. Recognize:

revenue for each performance obligation as it is being satisfied.

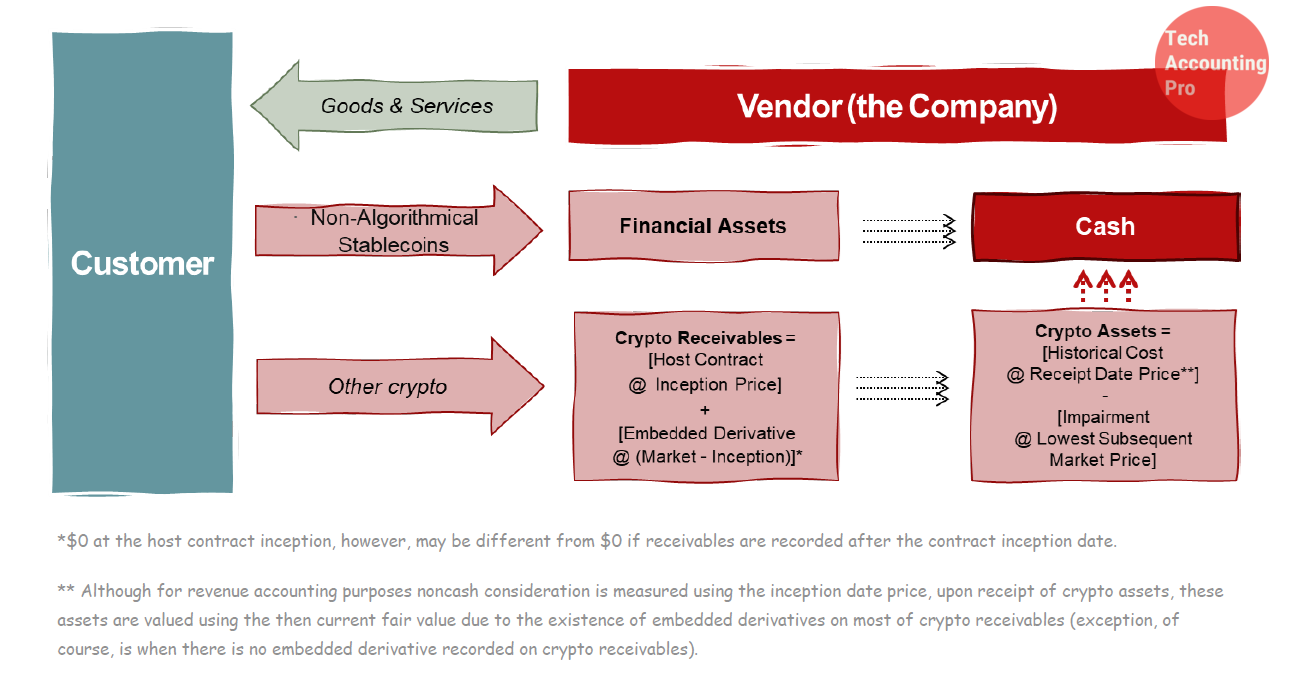

Consideration receivable

Crypto assets received or receivable from customers in exchange for satisfied performance obligations are treated as non-cash consideration under the revenue standard (ASC 606) while non-algorithmic stablecoins redeemable for cash (USDC, BUSD, USDT, etc.) are typically treated as financial assets.

Non-cash consideration is measured at its estimated fair value at the contract inception date. Hence, exchange-traded crypto assets receivable will be a hybrid instrument consisting of:

-

Host contract (Crypto assets receivable) – a non-financial asset to receive a specified number of crypto assets at a future date measured at the inception date of the contract.

-

Embedded derivative (Other Current/Non-current Assets/Liabilities) relating to the changes in market prices of crypto assets that are readily convertible to cash.

Embedded Derivatives

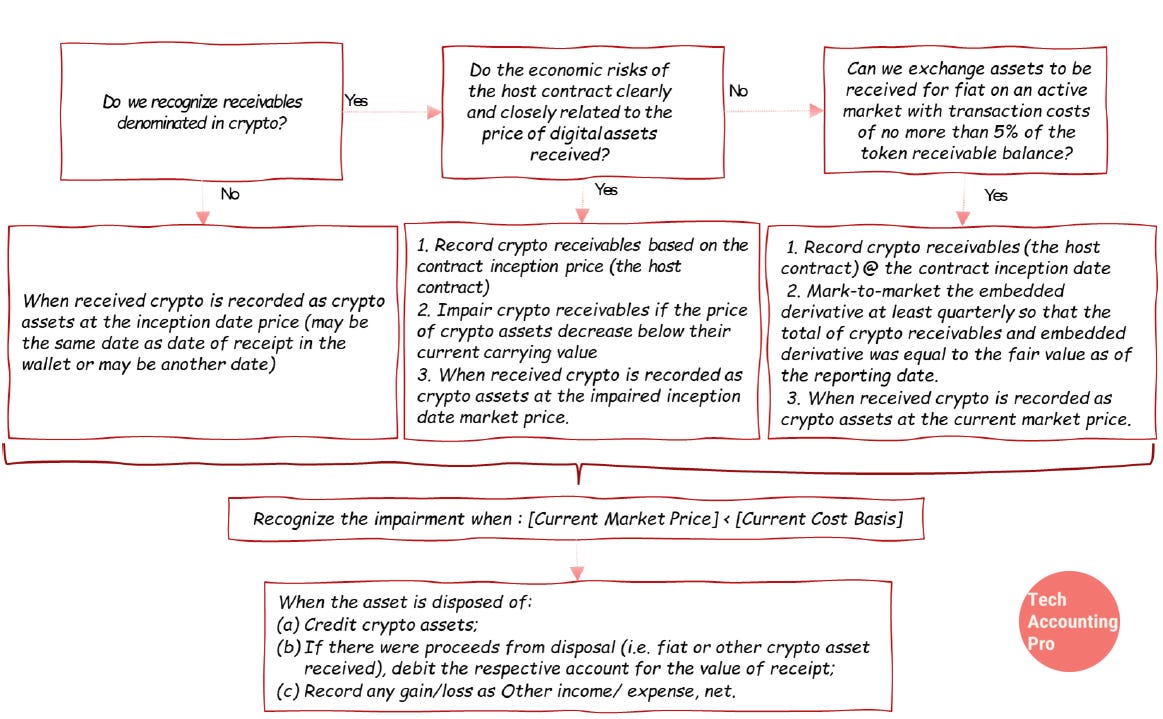

Embedded derivative typically exists based on the following criteria being met:

-

Notional (there is a fixed or determinable based on the contract number of tokens)

-

Underlying (which is the price of crypto assets on an active market)

-

Net settlement (if assets are traded on an exchange, these assets are readily convertible to cash, hence, the net settlement criterion is met )

Finally, in most of the vendor arrangements, the risks of the host (service) contract are not related to the risk of fluctuations in the prices of tokens received as consideration. If this is not the case and the risks of the embedded derivative are clearly and closely related to the risk of the host contract, the embedded derivative shall not be bifurcated.

Impairment

Crypto assets classified as intangible assets with an indefinite life are not amortized but assessed for impairment based on the pricing information from the principal or most advantageous market (using crypto asset sub-ledger software).

-

If conditions subsequently improve and the crypto value increases, the loss is NOT reversed, and

-

The impaired value remains the carrying value of the crypto until it is derecognized.

Settlement and derecognition

Once the crypto assets are received, we will record the crypto asset as an indefinite-lived intangible asset and derecognize the crypto assets receivable.

If an indefinite life intangible asset is sold for fiat, the counterparty identity and purpose determine the accounting treatment:

-

If sold to a customer, the sale is recorded as revenue under FASB ASC 606.

-

If the counterparty is not a customer, the gain/loss upon derecognition would be presented net, outside of revenue based on the applicable guidance:

-

If the transfer is in exchange for fiat, then the applicable guidance is FASB ASC 610-20, ‘Other Income – Gains and Losses from the Derecognition of Nonfinancial Assets’;

-

if the transfer is in exchange for another crypto or other non-financial assets, then the applicable guidance is FASB ASC 845, ‘Nonmonetary Transaction’

-

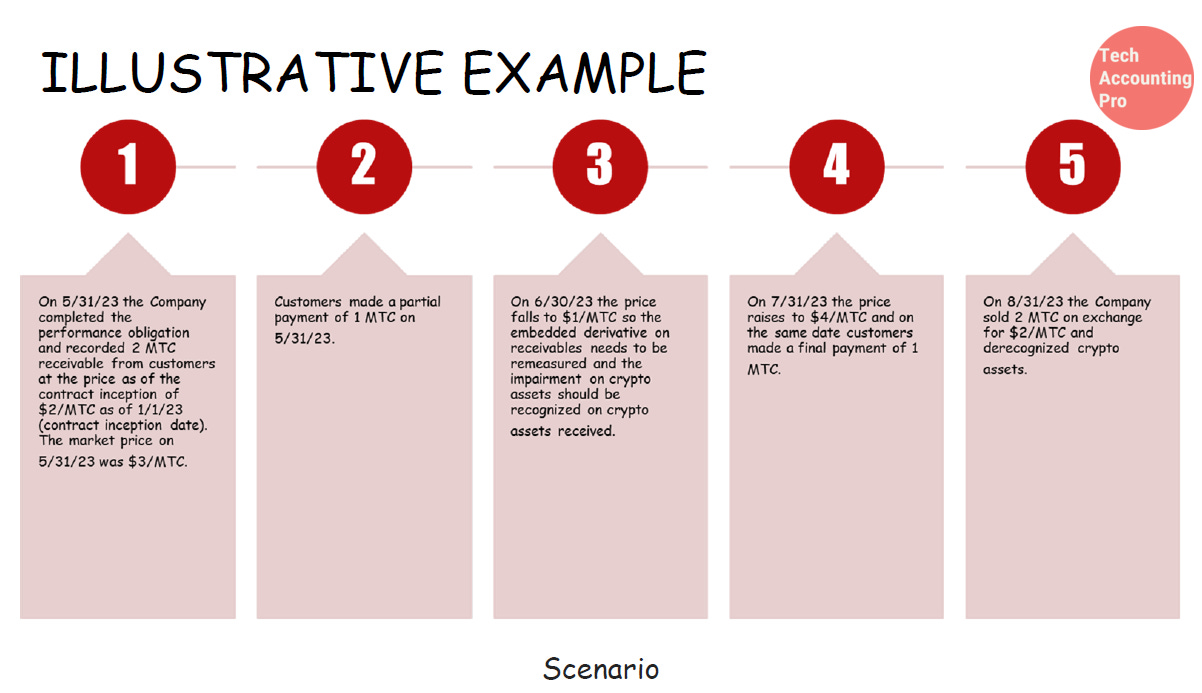

1-INITIAL MEASUREMENT

1a Revenue Recognition

On 5/31/23 we record 2 crypto assets revenue at $2/MTC which is the price as of 1/1/23 (the contract inception date):

Dr Receivable 2*$2

Cr Revenue 2*$2

1b Embedded Derivative

But the fair value on 5/31/23 was $3/MTC. We recognize the embedded derivative asset for $1 difference between current and contract inception date prices:

Dr Derivative asset 2*($3-$2)

Cr Unreal gain 2*($3-$2)

2-PARTIAL RECEIPT

On the same date we receive a partial payment of 1 MTC and recognize the crypto asset @$3 (the current active market price):

Dr Crypto Assets 1*$3

Cr Receivable 1*$2

Cr Realized gain 1*$1

Dr Unreal gain 1*$1

Cr Derivative asset 1*$1

Balance Sheet Values after the entries:

3-SUBSEQUENT MEASUREMENT

3a Remeasure Derivatives

On 6/30/23 the price is $1k/MTC, hence, we mark-to-market the embedded derivative to bring the Ending Derivative to $(1) (the liability position):

Dr Unrealized Loss 1*($1-$3)

Cr Derivative Asset 1*($3-$2)

Cr Derivative Liability 1*($2-$1)

3b Impairment for Crypto Assets

We record the impairment on the crypto assets received (intangibles):

Dr Impairment Expense 1*($3-$2)

Cr Crypto Assets 1*($3-$2)

Balance Sheet Values after the entries:

4-MARK-TO-MARKET

On 7/31/23 the price is $4/MTC. We cannot reverse the impairment, but we should mark-to-market the embedded derivative:

Dr Deritative asset 1*($4-$2)

Dr Derivative liability 1*($2-$1)

Cr Unrealized Loss 1*($4-$1)

Balance Sheet Values after the entries:

5-RECEIPT

On the same date, the customer transfers to the company the remaining 1 MTC due. We record 1 MTC received with the current value of $4:

Dr Crypto Assets 1*$4

Cr Receivable 1*$2

Cr Derivative asset 1*$2

Balance Sheet Values after the entries:

6-DERECOGNITION / CONVERSION

6a Impairment

On 8/31/23 crypto assets are sold for $2 each on exchange. The sale price is below the token costs. Hence, we first recognize the impairment.

Dr Impairment Expense 1*($4-$2)=$2

Cr Crypto Assets 1*($4-$2)=$2

Balance Sheet Values after the entries:

6b Derecognition

We record a net gain from cash proceeds of $4 less crypto assets costs on the balance sheet of $3 (after impairment):

Dr Cash 2*$2=$4

Cr Crypto Assets $1+$2=$3

Cr Other Income $4-$3=$1

Discover more from reviewer4you.com

Subscribe to get the latest posts to your email.