Why Blaming Shippers for Hanjin’s Demise is Ridiculous

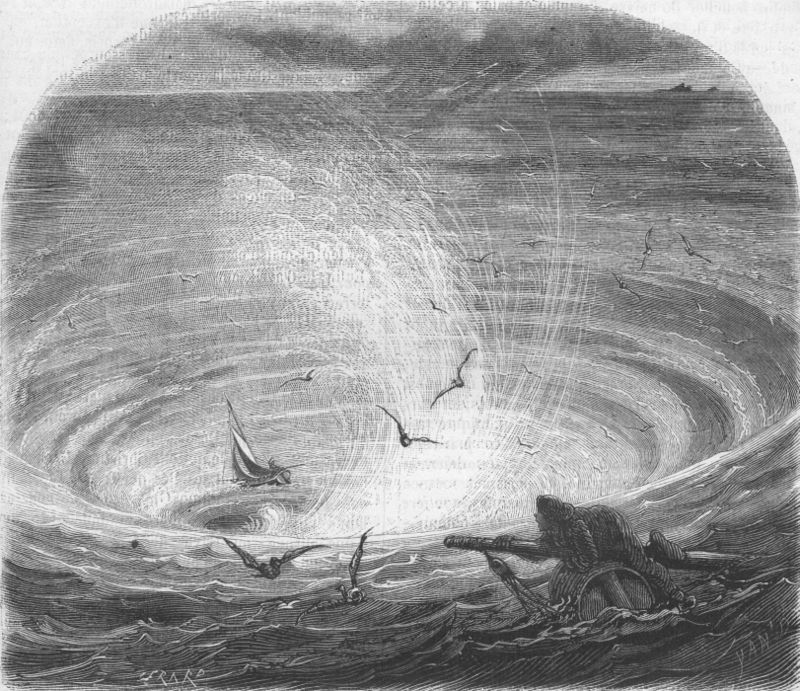

An illustration from Jules Verne’s essay “Edgard Poë et ses oeuvres” (Edgar Poe and his Works,1862) drawn by Frederic Lix or Yan’ Dargent

Following an analysis on Hanjin’s demise released by SeaIntel, shipping blogs and news sources are posting headlines laying responsibility for the major carrier’s bankruptcy on the shoulders of shippers.

The articles don’t put all the blame on shippers, but headlines like “Shippers ‘played a major role in Hanjin collapse’” from Lloyd’s Loading List certainly shade the situation with shippers being at fault.

Blaming Hanjin’s demise on shippers is ludicrous.

We’ll do future blogs discussing SeaIntel’s 33 page analysis on Hanjin’s collapse, but today we’ll talk about the topic of one small section of the analysis that inspired headlines like the one above.

The premise of the section is that shippers have a share in the blame of Hanjin’s collapse and carriers’ struggles in general.

Obviously, SeaIntel is not laying all the blame on shippers with the topic only getting a small section on page 9 of the analysis, and SeaIntel even acknowledges that the point of view might be controversial. I wouldn’t say controversial. I would say wrong.

The point the analyst makes can be understood; however, blaming shippers for Hanjin’s demise would be a very poor interpretation of the circumstances that led to the biggest bankruptcy in international shipping history.

Before I get into where the blame for Hanjin’s demise belongs, here is the section of SeaIntel’s analysis that points a finger a shippers:

It is clear that the shippers with cargo being caught up in this debacle have some tough challenges in the supply chains right now.

However, if we are being objective about this, the shippers are not without their part in creating this situation.

The relentless pressure on rates in recent years have created a situation where the entire carrier industry is heavily loss-making. And it is of course impossible to see a situation where you can both have a stable supply chain and at the same time ensure that the providers of said supply chain are loss making.

We are aware this might be a controversial point of view seen from shipper side, and we are not “blaming” them alone – it takes two to tango. Yes, the carriers have engaged in price wars, and it is the carriers that at times unprovoked offered even lower rates. But we are saying that an industry where one part obtains significant savings while the other part is loss making is not a set-up which is long-term viable.

Hence for the combined collective of global shippers they are facing a future where they have to start planning for increasing costs for ocean shipping compared to the current levels – the alternative is a situation where we will indeed again see large-scale supply chain disruptions.

So here’s the gist of this argument:

Low freight rates have made it difficult for carriers to make a profit, causing huge losses. These huge losses caused Hanjin’s collapse. Since shippers are accepting these low freight rates, even when they don’t cause them, shippers are partially to blame for carriers losing money and Hanjin’s demise.

The section also included the phrase “relentless pressure on rates” after saying “shippers are not without their part in creating this situation,” suggesting that this relentless downward pressure on freight rates comes from shippers.

Shippers did not create this downward pressure on freight rates.

Shippers are the consumers, so they absolutely want the lowest rates they can get. This is economics 101. Supply and demand. The consumer creates demand while looking for the best product or service at the best price.

Placing the blame on consumers for a business going out of business is crazy.

There are two places where the blame lies for carriers losing billions of dollars over the last several years and finally one of the major players going into bankruptcy: the carriers themselves and government interference.

The biggest fault falls on carriers. Carriers increased supply way over demand.

Grossly overestimating how much growth in demand the international shipping industry would experience, carriers invested obscenely in increasing capacity, and stampeded toward the creation and use of megaships. While it would be unfair to expect carriers to foresee the global recession that hit in 2009, which helped dropped demand way below expectations (and capacity), it is not unfair to call their business practices dubious.

I’m not even talking about carriers’ reputation for poor service or all the price fixing that major carriers have been found guilty of lately but of carriers ignoring the shipping industry’s needs that makes their actions dubious.

The decision to have megaships built in general was a bad move on the part of carriers. With ports around the world not equipped to handle the huge ships carriers have commissioned and put on the water, as well as the increase of shippers’ risk with having so much cargo on one ship, among other issues, the only ones who could have benefitted from megaships were carriers. It’s okay for businesses to make decisions that would benefit themselves (in this case, reducing costs by being able to move more cargo in single trips), but when not considering the needs of consumers and business partners (shippers and ports), such decisions often turn out poorly. And so it did for carriers.

The megaship trend became a series of really poor decisions by carriers when demand was obviously not increasing at expected rates, but carriers continued to invest heavily in having megaships built anyway. Because carriers were so enamored with these huge ships, they kept buying them when they didn’t really have the money, when the ships created huge amounts of overcapacity, and when the rest of the industry had to spend heavily and suffer congestion to handle the ships.

Carriers ballooned supply way over demand, creating the overcapacity problem that puts such heavy downward pressure on freight rates. Shippers didn’t do that.

It seems that the big carriers intentionally increased overcapacity to lower rates in order to drive out competition. The SeaIntel analysis’ section on shippers sharing the blame even mentions how carriers engaged in rate wars and “unprovoked offered even lower rates” to shippers.

Back in 2011, we posted a blog on Maersk smugly enduring low freight rates to outlast its competitors, in which its CEO was quoted as saying, “It would be natural if the smaller players in this business, or their banks, start questioning whether it’s a good idea to keep competing.”

Maersk is the biggest player in the international shipping industry when it comes to carrier capacity, so technically, that would make all the other carriers the smaller players in the business, no matter how big that carrier actually is.

While shippers are not to blame, the fault for this mess does not completely rest on carriers.

As years with carriers suffering billions of dollars in loss passed, many carriers should have gone under already. But through the years of poor business practices from carriers, governments have stepped in to bail the giant companies out, keeping them afloat.

Government interference allowed carriers to continue practicing business in ways that create giant money-sucking whirlpools without going under. But eventually a bank and government had to say enough is enough to throwing money away like dumping millions of dollars into the whirlpool of Charybdis.

And that’s why Hanjin collapsed.

Discover more from reviewer4you.com

Subscribe to get the latest posts to your email.