Organizing a chart of accounts is more art than science. There’s no one-size-fits-all method; the best approach is one that adapts to your business’s specific operations and nature. For deeper insights into this topic, check out publications by Deloitte, Harvard, OpenStax, SAP, and NetSuite.

Today, we’re focusing on organizing the chart of accounts for businesses that are actively transacting in cryptoassets.

1.1. Setting Goals

Many countries prescribe standardized charts of accounts; some of these can be modified, but the extent of permissible changes varies by country. In the US, entities are free to organize their charts of accounts without any restrictions. The main goal of the chart of accounts is to provide information at a level sufficient to:

-

Analyze business results to ensure effective operation and management

-

Standardize journal entry posting for routine processes

-

Comply with relevant tax and other regulatory reporting requirements

-

Prepare the financial statements and the related footnote disclosures

1.2. Defining Features

I want to emphasize that a chart of accounts, which consists of a list of synthetic accounts, is not the sole method for organizing data to achieve the aforementioned goals. These accounts can be enhanced and further disaggregated using features such as analytical accounts, dimensions, segments, cost elements, currencies, and variants.

Features may be:

-

Mutually exclusive (i.e., one line of the journal entry will always have only one value for the feature) or not (i.e., several tags may be used for the same individual line item at the same time)

-

Mandatory (i.e., each line item must have a value assigned to the feature), partially mandatory (i.e., only required for specific accounts or entities), or recommended. Mandatory features significantly affect the scalability of the system and the size of the database, so in practice, organizations typically have to limit the use of features to specified scopes and also keep organized data in the scope of each feature using consistent structures which may limit the data availability

1.3. Establishing Structure

It is a good practice to assign each account a unique numeric (or sometimes alphanumeric) identifier. This identifier should remain unchanged even if the account name is later modified to reflect the nature of the transactions recorded.

Companies may have multiple consolidated entities with different charts of accounts, so it is important to have the ability to map all of the individual charts of accounts to the unified consolidated chart that keeps the maximum level of details required.

Another good practice is to organize the accounts logically by categories of accounting objects these accounts are designed to track. Typically, the logical organization requires assigning sequential ranges of identification values to each category of accounting objects. Please see the following example for details:

1.4. Using Patterns

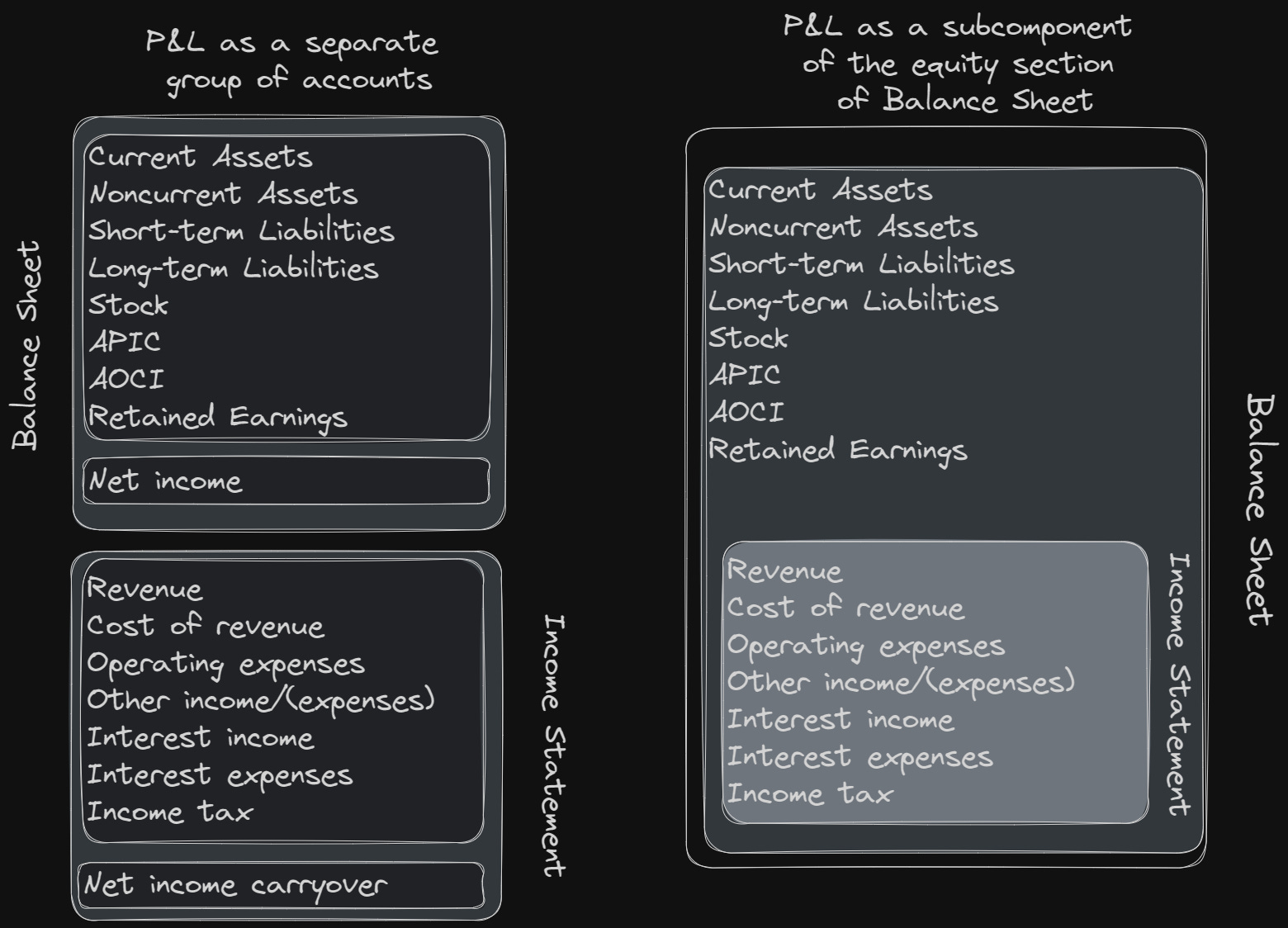

Typically, accountants prefer all account balances to net to zero at all times. There are two methods to include income statement accounts in the Chart of Accounts to achieve this:

-

As a subcomponent of the equity section

-

As a separate group of accounts

In addition, some accounting systems incorporate additional accounts designated for tracking of additional types turnover on income statement accounts. This allows accountants to track the structure of expenses first by nature and then by function as follows:

Debit SG&A

Credit Payroll Expense

Debit Payroll Expense

Credit Cash

Resulting turnovers of account “Payroll Expense” now can be used to accumulate all of the business payroll expenses regardless of the functional allocation of expenses. This may be helpful for analytical/disclosure purposes.

A similar approach can also be used to build up “Roll-forward” balance sheet accounts where sub-accounts represent separate activity categories for the roll-forward of the account balance. See an example below in the section where we discuss how to track digital asset balance sheet activity.

2.1. Relevant Features of Digital Asset Accounts

First, we can categorize crypto assets in the chart of accounts based on features that influence their recognition, measurement, derecognition, and presentation. The most relevant features, assuming significant engagement with each type of asset, include:

The suggested classification features include:

-

Applicable guidance that answers the question about what part of the codification guides the accounting for the crypto asset in question. We talked about examples of specific crypto assets in each category here, here, and here.

-

The presence of an active market dictates initial and subsequent measurement of the assets.

-

Restrictions on the transfer of assets allow for the segregation of restricted assets that need to be disclosed separately in the financial statements

-

Balance sheet classification determines whether assets should be presented as current or non-current on the company’s balance sheet as of the reporting date.

-

External cost basis and adjustments (intercompany profit, impairment, cumulative unrealized gain/loss) can be seggregated into separate accounts for reconciliation and disclosure purposes.

2.2. Balance Sheet Account Activity

Besides features of the assets themselves, it may be useful to split balance sheet account balances by activity types at the level you need to prepare a roll forward schedule.

Since most modern accounting systems do not use the red storno method for entry reversal, the debit and credit turnovers of balance sheet accounts have no practical meaning. This happens because reversing erroneously posted debits artificially inflates credit turnovers and vice versa. One possible way to address this issue is by splitting balance sheet accounts into subaccounts used to track specific types of activities reflecting transactions posted to the underlying balance sheet accounts. An illustrative list of possible dimensions is presented below:

This approach necessitates that digital assets account balances be reformed annually at the end of the Company’s fiscal year.

2.3. Accounts Receivable/Payable

Additionally, consider the impact on crypto accounts receivable and payable:

This also applies to related embedded derivatives:

3.1. Operating Costs

Common examples of crypto specific accounts include:

-

Transaction fees

-

Test sends

Crypto-native companies seldom sell physical goods and generally do not engage in business activities that necessitate the allocation of periodic costs between expenses and work-in-progress (there are some exceptions to this rule – such as Core Scientific Inc. – depending on specifics of the business, but these exceptions are less common).

As a result many crypto native businisses charge operating costs incurred during the period directly to operating expenses. It is very uncommon to see the caption “Cost of sales” in the income statement of a non-diversified crypto native business.

3.2. Realized and Unrealized Gains/(Losses)

Five separate accounts are required to track the measurement results of crypto assets under FASB ASC 350-80 (crypto asset guidance/fair value model) and FASB ASC 350-30 (intangible assets guidance/impaired costs model):

In addition to this, separate accounts are typically used for realized and unrealized gain/(loss) on embedded derivative assets and liabilities.

Please share other best practices for designing crypto native charts of accounts in the comments below.

Discover more from reviewer4you.com

Subscribe to get the latest posts to your email.