I analyzed US public companies with significant Bitcoin mining operations to determine the accounting policies these companies apply, identify where they follow a standard approach, and highlight where I see the biggest differences in viewpoints.

I selected companies for this study by looking into lists of public US companies engaged in the crypto mining business from several industry studies of which I was aware. The most well-known is the NBER working paper “Bitcoin Mining Meets Wall Street: A Study of Publicly Traded Crypto Mining Companies” by Hanna Halaburda & David Yermack, which lists thirteen companies, including seven US-based companies. I included in my sample only the seven companies that follow US GAAP accounting rules:

-

Riot Platforms Inc. (RIOT)

-

CleanSpark Inc. (CLSK)

-

Marathon Digital Holdings Inc. (MARA)

-

Cipher Mining Technologies Inc. (CIFR)

-

Greenidge Generation Holdings Inc. (GREE)

-

TeraWulf Inc. (WULF)

-

Core Scientific Inc. (CORZ)

However, while gathering data on the Bitcoin production numbers from Mining Magazine and research published by Compass Mining, I identified several more US-listed companies engaged in Bitcoin mining:

-

Stronghold Digital Mining, Inc. (SDIG)

-

Hut 8, Inc. (HUT8)

-

Mawson Infrastructure Group, Inc. (MIGI)

-

Soluna Holdings, Inc. (SLNH)

I also searched the SEC EDGAR portal for any annual filings of Form 10-K containing “bitcoin mining” and discovered two more companies actively engaged in the Bitcoin mining business:

-

GRIID Infrastructure Inc. (GRIID)

-

Ault Alliance, Inc. (AULT)

Additionally, I was aware of one Bitcoin mining company that had started the listing process a few years ago but subsequently withdrew the application. However, as their financial statements were prepared under US GAAP and were available via EDGAR, I included this company in my research:

All of the companies I studied participated in mining pools, with fees calculated using the FPPS method. I also encountered companies using multiple pools with different methods for fee calculation, as well as one company that managed their own mining pool.

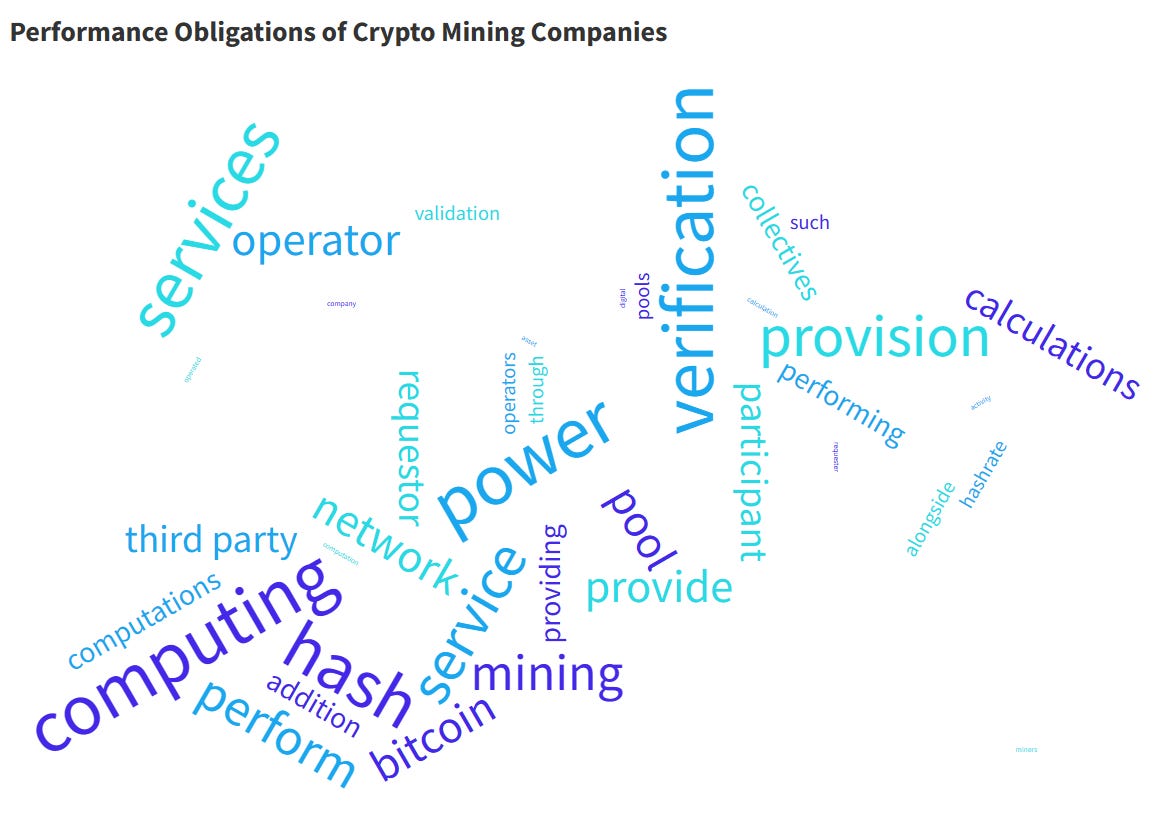

Because of the commonality, each bitcoin miner identified its performance obligation in a similar manner using similar words. I used a word cloud below to visualize these definitions.

Interestingly, no company has discussed why digital assets are not viewed as an output of the primary activity of Bitcoin miners and why parties contracting to purchase this output do not meet the definition of a customer.

Mining pool fees

Very few companies disclosed the amount of mining pool operator fees. However, I noted a drastic difference in the fees of mining pool operators. Additionally, Cipher Mining Technologies, Inc. and TeraWulf, Inc. disclosed that they used the Foundry USA mining pool in 2023. The minimum fees disclosed were 0.3% (Ault Alliance) with a maximum of 2% (Riot Platforms). Potential savings for Riot Platforms in 2023 alone could amount to $5.6 million if they used the pool with lower fees, assuming all other variables remained the same.

Six Bitcoin miners explicitly disclosed the accounting policy to present the crypto mining revenue net of their mining pool fees because they treated such fees as consideration paid to a customer without any distinct goods or services received in exchange for the payment made. The remainder of our sample did not state their policy explicitly.

I analyzed the structure of the cost of mining revenue and noted that only three companies included Depreciation and Amortization in Costs of Revenue, while others excluded these amounts. Additionally, only Core Scientific, Inc. explicitly stated that they included stock-based compensation in costs of revenue, while other companies in our sample did not discuss whether this component is included in their costs.

Most companies in our sample depreciate crypto mining equipment over a 3-year estimated useful life period. The useful lives observed ranged from 1 to 5 years.

All companies I studied recorded digital assets as current assets, although two companies segregated a portion of digital assets as non-current. Below are excerpts from the accounting policies of these two companies:

Hut 8 accounting policy:

“The Company’s treasury strategy is to cover its operating costs through the selling of digital assets earned from its revenue activities. These digital assets are included in current assets in the Consolidated Balance Sheets due to the Company’s ability to sell them in a highly liquid marketplace and the Company reasonably expects to liquidate these digital assets to support operations or for treasury management within the next 12 months.

The Company’s remaining digital assets held are included in non-current assets as this portion of digital assets is not reasonably expected to be sold in the next 12 months as it is outside of the 12-month expected utilization for operational and capital needs of the Company.”

[Hut 8 Form 10-K for the year ended 12/31/23]

Marathon Digital Holdings accounting policy:

“Digital assets are included in current assets in the Consolidated Balance Sheets due to the Company’s ability to sell bitcoin in a highly liquid marketplace and the sale of bitcoin to fund operating expenses to support operations. In addition, digital assets provided as collateral for long-term loans were reported as Digital assets, restricted at December 31, 2022 and classified as long-term assets in the Consolidated Balance Sheets.”

[Marathon Digital Holdings Form 10-K for the year ended 12/31/23]

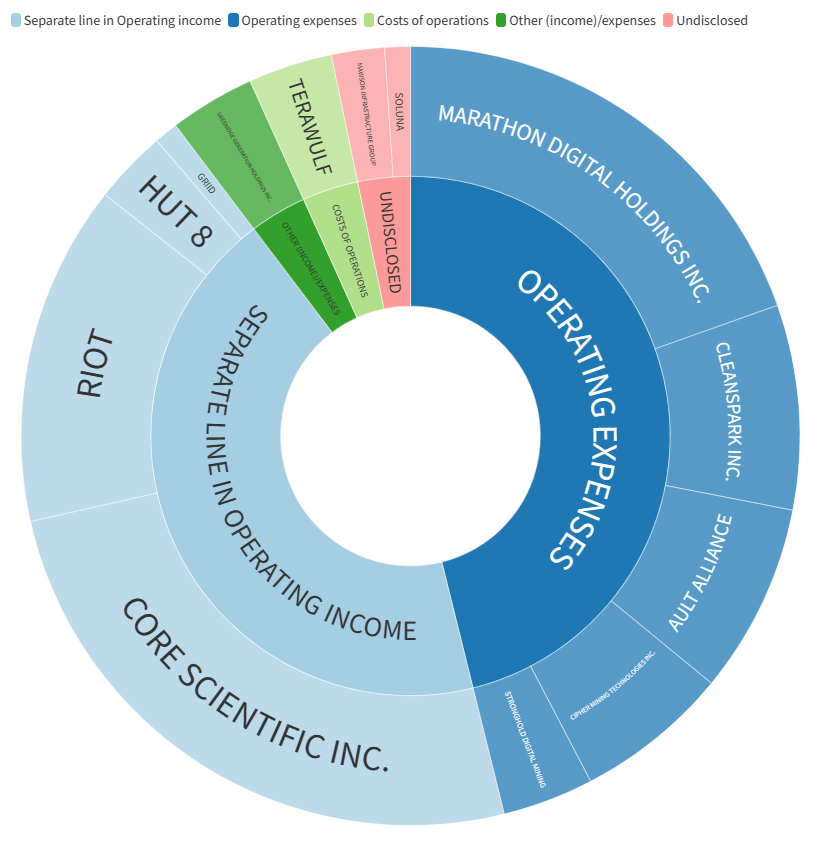

Most companies I studied recorded gains/losses on digital assets either as an item of operating expenses or a separate line item included in the calculation of Operating Income. Only one company (GREE) recorded gains/losses on digital assets as part of Other Income/(Expense), outside of Operating Income/(Loss).

Among the companies surveyed:

-

Five recorded proceeds from Bitcoin sales as operating cash flows.

-

Four recorded proceeds from Bitcoin sales as investing cash flows.

-

Two recorded proceeds from sales that occurred within a short timeframe from receipt of assets as operating cash flows, but outside of this short timeframe, any proceeds were recorded in investing cash flows.

In addition, three companies disclosed their policy for classifying cash outflows related to purchases of digital assets – Riot Holdings presented purchases of digital assets as Operating cash flows, while two other companies presented the same activity as investing cash outflows.

I also took a brief look at the status of adoption of the new crypto accounting standard as shown in the table below:

Finally, I also identified several accounting policies that I only saw in one of the surveyed company financials without any similar policy being disclosed by any of its peers. I carried over quotes from relevant disclosures below:

Core Scientific Inc.

“Digital assets that are purchased in an exchange of one digital asset for another digital asset are recognized at the fair value of the asset surrendered.”

Marathon Digital Holdings Inc.

“Operator

From September 2021 until May 2022, the Company engaged unrelated third-party mining enterprises (“pool participants”) to contribute hash calculations, and in exchange, remitted transaction fees and block rewards to pool participants on a pro rata basis according to each respective pool participant’s contributed hash calculations. The MaraPool wallet (owned by the Company as Operator) is recorded on the distributed ledger as the winner of proof of work block rewards and assignee of all validations and, therefore, the transaction verifier of record. The pool participants entered into contracts with the Company as Operator; they did not directly enter into contracts with the network or the requester and were not known verifiers of the transactions assigned to the pool. As Operator, the Company delegated mining work to the pool participants utilizing software that algorithmically assigned work to each individual miner. By virtue of its selection and operation of the software, the Company as Operator controlled delegation of work to the pool participants. This indicated that the Company directed the mining pool participants to contribute their hash calculations to solve in areas that the Company designated. Therefore, the Company determined that it controlled the service of providing transaction verification services to the network and requester. Accordingly, the Company recorded all of the transaction fees and block rewards earned from transactions assigned to MaraPool as revenue, and the portion of the transaction fees and block rewards remitted to MaraPool participants as cost of revenues.

In accordance with ASC 606-10-32-21, the Company measures the estimated fair value of the non-cash consideration (block reward and transaction fees) at contract inception, which is at the time the performance obligation to the requester and the network is fulfilled by successfully validating a block. The Company measures the non-cash consideration which is fixed as of the inception of each individual contract using the quoted spot rate for bitcoin determined using the Company’s primary trading platform for bitcoin at the time the Company successfully validates a block.”

Cipher Mining Technologies Inc.

“Bitcoin awarded to the Company as distributions-in-kind from equity investees are accounted for in accordance with ASC 845, Nonmonetary Transactions, and recorded at fair value upon receipt.”

TeraWulf, Inc.

“The Company has adopted an accounting policy to aggregate individual contracts with individual terms less than 24 hours within each intraday period.”

“The Company accounts for goods and services exchanged in nonmonetary transactions at fair value unless the underlying exchange transaction lacks commercial substance or the fair value of the assets received or relinquished is not reasonably determinable, in which case the nonmonetary exchange would be measured based on the recorded amount of the nonmonetary asset relinquished.”

Soluna Holdings, Inc.

“The Company’s equipment miners are classified in Level 2 of the fair value hierarchy due to the quoted market prices for similar assets.”

Discover more from reviewer4you.com

Subscribe to get the latest posts to your email.